Eye2Scan & Infolegale: Transforming Occupational Fraud Detection Through Dual-Layer Monitoring...

As many other fields, Internal audit is experiencing a profound digital transformation that's reshaping professional practices across the sector. Traditional methods used by Internal Audit departments are being challenged, while new technologies create unprecedented opportunities to enhance effectiveness. Advanced analytics now make a complete overhaul of fraud detection and risk monitoring approaches not just possible, but essential to meet today's business requirements.

Understanding Automated Controls and Continuous Monitoring in Modern Internal Audit

What Are Automated Controls?

Automated controls are programmed mechanisms that check compliance with established rules and procedures in real-time or at regular intervals. Unlike manual controls requiring human intervention, these systems work autonomously using algorithms and predefined parameters.

These controls can be:

- Preventive: blocking non-compliant transactions before they're completed

- Detective: identifying anomalies after they occur

- Predictive: anticipating potential risks by analyzing behavioral patterns

Continuous Monitoring: A Paradigm Shift in Internal Audit Methodology

Continuous monitoring marks a major evolution from traditional periodic audits. This approach, primarily implemented by internal control teams working in synergy with internal audit, involves:

- Analyzing data in real-time or near real-time

- Monitoring all transactions rather than just samples

- Immediately detecting exceptions and anomalies

- Enabling rapid responses to identified risks

This method transforms the control cycle by allowing internal auditors to leverage existing monitoring systems, evaluate their effectiveness, and focus their efforts on uncovered risk areas or more strategic analyses.

The Current State of Technology in Fraud Detection and Internal Audit

Widespread Adoption of Data Analysis Tools

According to the ACFE's "Anti-Fraud Technology Benchmarking Report, 91% of organizations now use data analysis techniques in their anti-fraud programs. This widespread adoption stems from clear advantages:

- Increased volume of monitored transactions

- Faster fraud detection

- Automation of time-consuming tasks

Data analysis enables organizations to examine vast amounts of information to identify patterns, trends, and anomalies that would be invisible to the human eye. These tools can flag suspicious transactions, unusual behaviors, or potential control violations in ways that manual review simply cannot match.

Transformative Technologies for Internal Audit Departments

The Institute of Internal Auditors (IIA)'s "Vision 2035" study highlights three key technologies shaping the future of internal audit:

- Data Analysis (91% of respondents): Deep data exploration generating strategic and operational insights.

- Continuous Monitoring (79%): Systems that enable ongoing control of processes and transactions.

- Automation (76%): Programmed handling of repetitive tasks that frees up human resources and reduces errors.

These technologies are converging to create a more dynamic, proactive, and effective audit environment—one centered on risk analysis rather than manual transaction verification. Robotic Process Automation (RPA) plays a particularly important role in this transformation, as it allows audit teams to automate routine data collection and testing procedures that previously consumed significant staff hours.

Challenges in the Digital Transformation of Internal Audit Programs

Despite the clear benefits, several key obstacles are slowing the adoption of fraud detection technologies and hindering the full potential of internal audit's digital transformation:

1. Budget Constraints and Limited Resources

The ACFE report reveals that 82% of organizations cite budget constraints as a major barrier to adopting new anti-fraud technologies. Developing customized solutions is particularly expensive, both in terms of financial investment and human resources.

2. The Problem with In-House Solutions for Audit Analytics

Many organizations still rely on internally developed platforms using tools like Excel and Power BI. This approach creates several problems:

- Operational silos that limit information sharing

- Inefficient, fragmented, and non-optimized systems

- Extended project timelines with high development costs

- Dependency on specialized IT and data analysis expertise

- Higher risk of human error in tool design and operation

These homegrown solutions, while designed to meet specific needs, typically lack the flexibility and scalability of specialized platforms. They're also often expensive and time-consuming to implement.

3. Managing False Positives in Automated Fraud Detection

A major challenge with automated detection systems is the high rate of false positives—alerts triggered by legitimate but unusual transactions. Too many false positives quickly overwhelm teams and dilute attention from genuine anomalies that require investigation.

4. The Challenge of Data Reliability and Digital Trust in Audit Technology

Building trust in results generated by automated systems remains a significant hurdle. Auditors accustomed to manual verification often hesitate to rely on algorithmic conclusions, particularly when the underlying data's integrity isn't guaranteed. This makes rigorous data governance essential to digital transformation success.

5. The Complexity of Heterogeneous IT Infrastructures

System fragmentation presents another significant obstacle. Large companies typically operate with multiple ERP systems resulting from mergers and acquisitions, alongside various specialized business applications. This diversity complicates the implementation of continuous monitoring solutions that require centralized data access.

The Future of Internal Audit's Digital Transformation

The digital transformation of internal audit isn't just about technology—it's a complete redesign of the approach:

From Sampling to Exhaustive Analysis in Modern Audit Methodology

Today's advanced analytics tools allow organizations to examine every transaction rather than limited samples. This evolution now includes transversal controls that correlate data across different modules and establish connections between anomalies. The result: high-criticality alerts with fewer false positives. This approach benefits both internal audit teams targeting investigations and internal control teams conducting daily monitoring.

From Periodic Audit to Enhanced Collaboration with Internal Control

Digital transformation is redefining how audit and internal control teams work together. Audit identifies priority risks during its missions, then partners with internal control to ensure continuous monitoring. This collaborative model allows auditors to effectively delegate follow-up through automated controls while focusing on higher-value activities like performance audits.

De la détection réactive à la prévention proactive

L'intelligence artificielle permet non seulement de détecter les fraudes mais aussi de les prévenir. L'approche hybride combinant contrôles "rule-based" et le machine learning est devenue essentielle pour une couverture complète : les règles vérifient la conformité aux critères établis tandis que l'IA détecte des schémas complexes et anomalies subtiles impossibles à programmer manuellement.

From Reactive Detection to Proactive Prevention Through Audit Technology

AI now enables not just fraud detection but prevention. The hybrid approach combining rule-based controls with machine learning has become essential for comprehensive coverage. Rules verify compliance with established criteria, while AI identifies complex patterns and subtle anomalies that would be impossible to program manually.

RPA-enabled audit solutions further enhance this capability by continuously monitoring key risk indicators and control points across business processes. By deploying RPA bots to perform consistent checks based on predefined rules, organizations can maintain vigilance across their operations without increasing headcount or auditor workload.

From Isolated Analysis to a Comprehensive Vision of the Enterprise

Modern platforms integrate directly with information systems, enabling systematic comparison across entities, countries, business units, and accounting structures. This centralization makes it easier to identify best practices, detect anomalies against internal benchmarks, and progressively harmonize processes organization-wide.

The Eye2Scan Solution: The Alliance of Technology and Expertise for Internal Audit Excellence

Addressing these challenges head-on, Eye2Scan offers an integrated approach designed specifically for modern Internal Audit and Internal Control departments. The Eye2Scan platform:

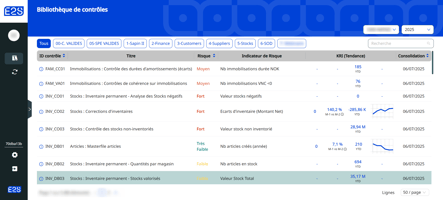

- Connects directly to ERP systems and business applications, providing immediate access to all relevant data—creating a true control data lake

- Includes a comprehensive library of pre-programmed controls based on industry best practices and key business cycles (P2P, O2C, R2R, SOD...)

- Features customization options that minimize false positives

- Offers an intuitive interface requiring no specialized ERP or data analysis expertise

- Delivers traceable follow-up of detected anomalies, facilitating regulatory compliance

- Ensures robust data security and governance to maintain data integrity

By choosing Eye2Scan, organizations avoid the lengthy, complex, and expensive process of developing internal solutions. Instead, they gain an automated, efficient tool for risk-based audit controls—all the advantages without the usual drawbacks.

As the digital transformation of internal audit reshapes the profession, practitioners must equip themselves with the right tools to meet current and future challenges. By combining data analysis, continuous monitoring, and automation, audit departments can improve operational efficiency while strengthening their strategic contribution to the organization.

This evolution aligns perfectly with the new Internal Audit Standards established by the IIA, which emphasize the growing importance of technological resources in professional practice. The digital transformation of internal audit represents a unique opportunity to redefine the value this essential function delivers to organizations worldwide.